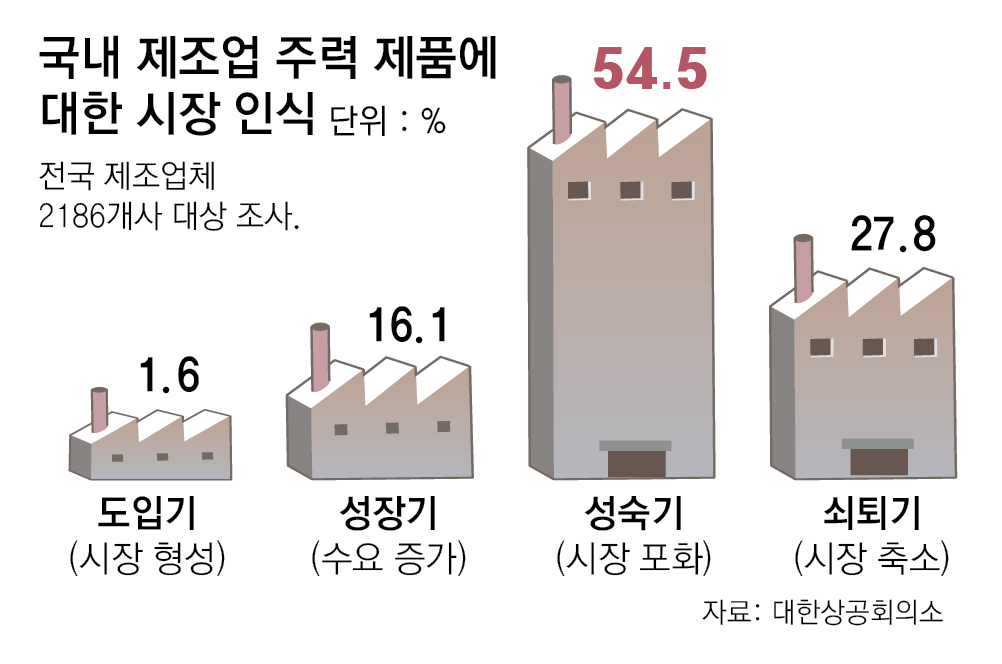

A survey by the Korea Chamber of Commerce and Industry (KCCI) reveals that 82.3% of South Korean manufacturers believe their main product markets have entered a 'red ocean' of fierce competition, with 83.9% admitting they have no advantage or have been overtaken by rivals. The findings underscore a structural crisis in steel, petrochemicals, and other export-driven sectors, largely due to oversupply from China and a lack of innovation in new industries like AI and secondary batteries. For overseas buyers, this signals potential shifts in pricing, supply reliability, and sourcing strategies from South Korea.

Red ocean across key industries

Non-metallic minerals (cement, etc.) topped the list at 95.2%, followed by oil refining and petrochemicals at 89.6%, steel at 84.1%, machinery at 82.9%, textiles at 82.4%, and automotive and parts at 81.2%. These sectors, which have driven South Korea's export growth since the 1960s, are now facing market saturation or decline, according to the companies' own assessments.

Steel sector hit hard by Chinese oversupply

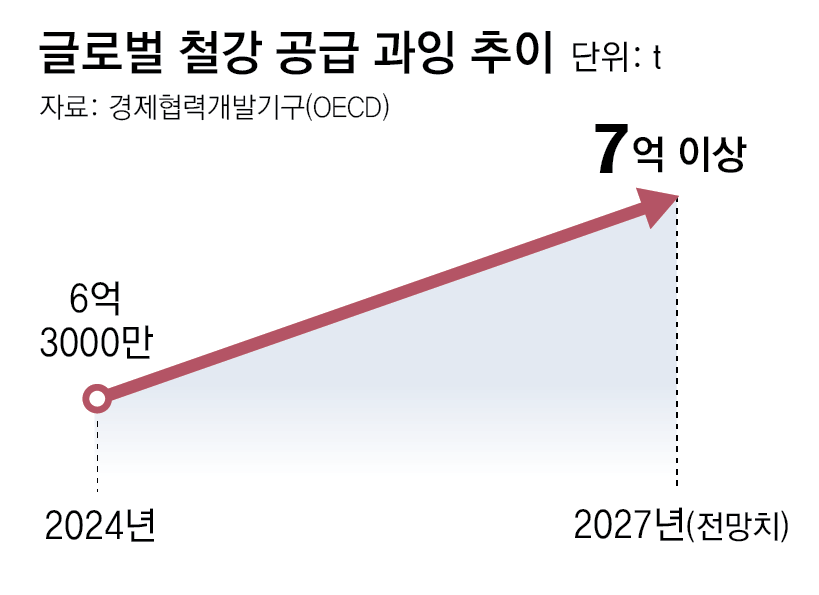

South Korean steelmakers have seen their global influence shrink sharply due to China's supply glut. OECD data shows global steel oversupply reached 630 million metric tons last year—10 times South Korea's annual output of 63 million tons. In response, 106 lawmakers from both ruling and opposition parties jointly proposed the 'K-Steel Act' on April 4, offering subsidies, tax breaks, and loans to support the industry. Meanwhile, domestic special steel producers like SeAH Besteel and SeAH Changwon Special Steel have filed anti-dumping complaints with the Korea Trade Commission against Chinese special steel bars, as their operating profits have plunged over 90% in two years.

Petrochemicals face structural oversupply

South Korea's petrochemical industry is also grappling with oversupply from the Middle East and China, prompting forecasts of capacity cuts and restructuring. Boston Consulting Group projects that 15 million metric tons of new ethylene and commodity polymer capacity will come online in the next 2-3 years, with oversupply persisting through 2030. This trend could pressure margins for Korean producers and affect global pricing dynamics for polymers and basic chemicals.

Innovation gap and lack of new business investment

Experts attribute the manufacturing slump to a reluctance to venture into new businesses. While the U.S. pivoted to IT before losing its industrial edge, South Korea failed to invest aggressively in alternative industries when its traditional sectors were still strong. The KCCI survey found that 57.6% of manufacturers have no ongoing new business projects, citing financial difficulties (25.8%) and lack of confidence in market viability (25.4%) as key barriers. Professor Kim Jeong-ho of KAIST stressed the need for AI and robotics to boost productivity, calling for government support in infrastructure.

What buyers should watch

Overseas importers and distributors should monitor South Korea's policy response, including the K-Steel Act's implementation, which could affect steel export prices and availability. The anti-dumping actions on Chinese special steel may lead to trade disputes and supply shifts. In petrochemicals, prolonged oversupply may create buying opportunities but also risks of plant closures. The broader innovation deficit suggests South Korea may struggle to maintain its competitive edge in high-value chemicals, potentially opening doors for alternative suppliers in China and the Middle East.

Source: Read the original report | Published: August 05, 2025