China's prolonged deflation and weak domestic demand are forcing Taiwanese companies heavily invested in the mainland to restructure or exit unprofitable ventures. Taiwan Glass's flat glass and soda ash operations are deep in the red, with only its fiberglass fabric business providing a lifeline. Meanwhile, Win Semiconductors is cutting losses on its decade-long pig farming venture to refocus on its core gallium arsenide wafer foundry business. These developments signal growing risks for chemical and industrial material suppliers tied to China's construction and agricultural sectors.

Taiwan Glass: Soda Ash Turns Sour

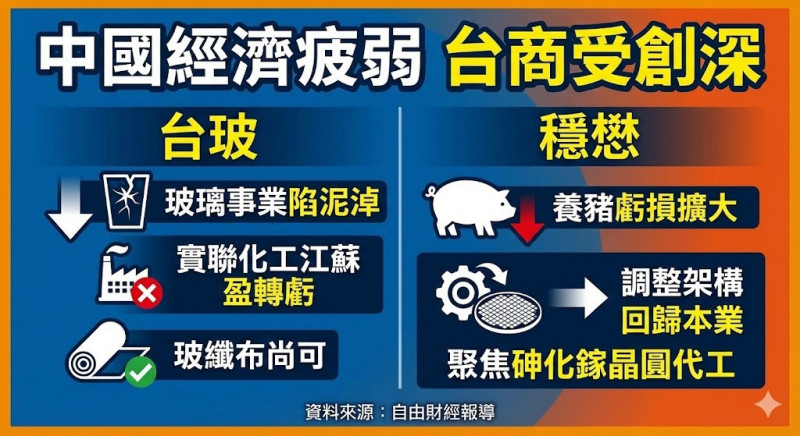

Taiwan Glass, which has nearly all its overseas investments in China, reported a NT$1.45 billion loss from its Chinese subsidiaries in Q3 2025, similar to the NT$1.47 billion loss a year earlier. While the company posted a small EPS of NT$0.1, ending six consecutive quarterly losses, this was solely due to AI-driven demand boosting fiberglass fabric prices and shipments. Its core glass businesses remain a drag.

The company's flat glass and low-emissivity glass operations continue to lose money. More notably, Shihlien Chemical Jiangsu, its soda ash production unit and former cash cow, swung from a NT$160 million profit in the first three quarters of 2024 to a NT$370 million loss in the same period of 2025. This marks the first-ever loss for the soda ash venture, reflecting the severe downturn in China's construction and real estate sectors.

Fiberglass Fabric: A Rare Bright Spot

Taiwan Glass's fiberglass fabric subsidiaries—Taijia Chengdu Fiberglass, Taijia Glass Fiber, and Taijia Bengbu Glass Fiber—collectively turned around from a NT$790 million loss in the first three quarters of 2024 to a NT$83.2 million profit in the same period of 2025. The recovery is attributed to rising demand from AI-related PCB manufacturing, which has lifted both unit prices and shipment volumes for fiberglass fabric.

Win Semiconductors: Exiting Pig Farming After Nearly NT$7.5 Billion Burn

Win Semiconductors, a gallium arsenide wafer foundry, entered China's pig farming business nearly a decade ago with investments totaling NT$9.517 billion. By the end of Q3 2025, the book value of these investments had shrunk to just NT$2.023 billion, implying losses of nearly NT$7.5 billion. In the first three quarters of 2025 alone, the company recognized NT$2.59 billion in losses from its China operations, more than double the NT$1.05 billion loss in the same period of 2024.

The main culprit is Jiangsu Quanwen Agriculture Technology, which reported a loss of NT$1.53 billion in H1 2025 but saw that balloon to NT$15.08 billion by Q3, with its book value turning negative at NT$1.139 billion. In late 2025, Win Semiconductors announced a debt-to-equity swap, issuing new shares to transfer equity in its Chinese subsidiaries. Market analysts view this as a decisive move to cut losses and refocus on its core semiconductor business.

What Buyers Should Watch

For overseas buyers of soda ash, flat glass, and fiberglass fabric, the ongoing restructuring at Taiwan Glass signals potential supply shifts. The soda ash loss may lead to reduced output or price adjustments, while fiberglass fabric supply could tighten further if AI demand continues. For gallium arsenide wafer users, Win Semiconductors' retreat from pig farming means the company will likely allocate more resources to its foundry services, potentially improving capacity and lead times. Importers of agricultural chemicals and feed additives should note the broader deflationary pressure on China's pig farming sector, which may reduce demand for related inputs.

Source: Read the original report | Published: January 10, 2026