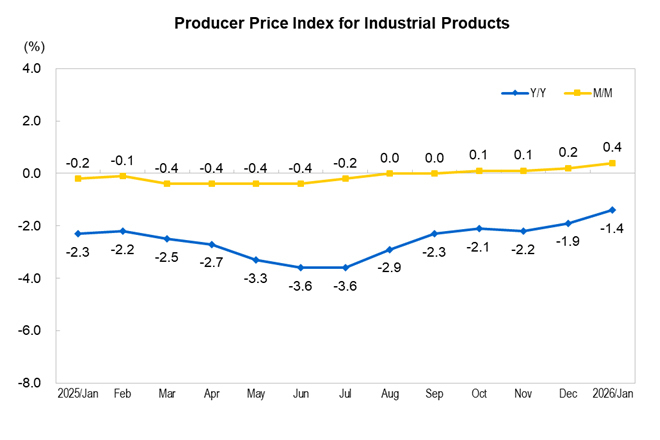

China's January 2026 industrial producer price index (PPI) fell 1.4% year-on-year, narrowing by 0.5 percentage points from December, while month-on-month it rose 0.4%, according to official data released February 12. For chemical buyers, the purchasing price index for raw chemical materials dropped 5.8% YoY but edged up 0.1% month-on-month, signaling persistent deflationary pressure in the sector. Meanwhile, nonferrous metals and cables posted a sharp 16.1% YoY increase, driven by strong demand and supply constraints.

Key chemical-sector price movements

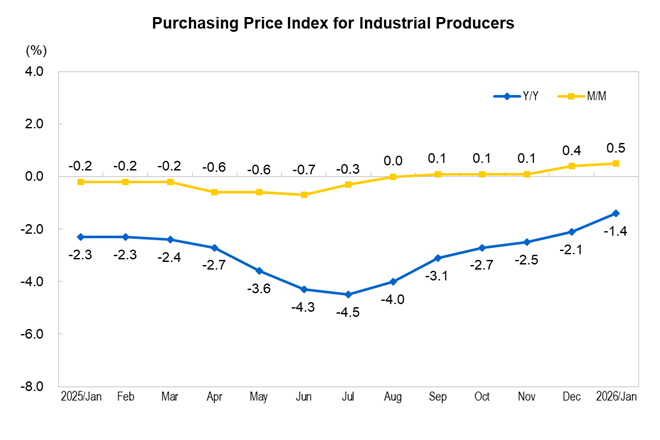

Among purchasing price indexes for industrial producers, fuel and power fell 7.1% YoY and 0.7% month-on-month. Building materials and non-metals declined 4.7% YoY and 0.6% month-on-month. Ferrous metals and agricultural products both dropped 2.9% YoY, while textile materials fell 2.2% YoY. Nonferrous metals and cables rose 16.1% YoY and 4.5% month-on-month, reflecting sustained upward momentum.

Downstream manufacturing cost signals

In the producer price indexes for major industries, manufacture of raw chemical materials and chemical products fell 5.0% YoY but rose 0.6% month-on-month. Manufacture of chemical fibers dropped 6.4% YoY and 0.4% month-on-month. Manufacture of medicines declined 4.4% YoY and 0.9% month-on-month. These figures indicate ongoing cost relief for buyers of commodity chemicals, but mixed signals for specialty segments.

What buyers should watch

Importers of Chinese chemical raw materials should note the continued year-on-year price declines, which may offer short-term procurement advantages. However, the month-on-month uptick in raw chemical materials (0.1%) and the sharp rise in nonferrous metals suggest that input costs may be bottoming out. Buyers should monitor the narrowing PPI decline and potential upward pressure on chemical prices in coming months, especially for nonferrous-related intermediates.

China sourcing context

The data, published by China's National Bureau of Statistics, covers January 2026. The overall PPI decline of 1.4% YoY, though narrowing, remains in deflationary territory, reflecting weak domestic demand and global oversupply in many chemical segments. For overseas buyers, this environment supports competitive pricing from Chinese suppliers, but logistics and trade policy factors should also be considered in sourcing decisions.

Source: Read the original report | Published: February 12, 2026