Europe's chemical industry is facing an unprecedented contraction, with plant closures surging sixfold since 2022 and new investments plummeting by 86% in the last year, according to a new study by Roland Berger commissioned by CEFIC. For overseas buyers, this signals tightening supply of key petrochemicals, polymers, and inorganics, potential price volatility, and a need to reassess European sourcing strategies as the region's production base shrinks.

Closure crisis deepens

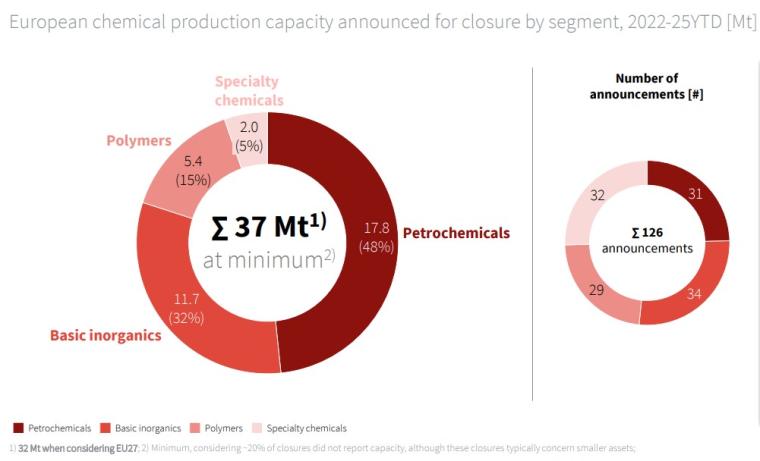

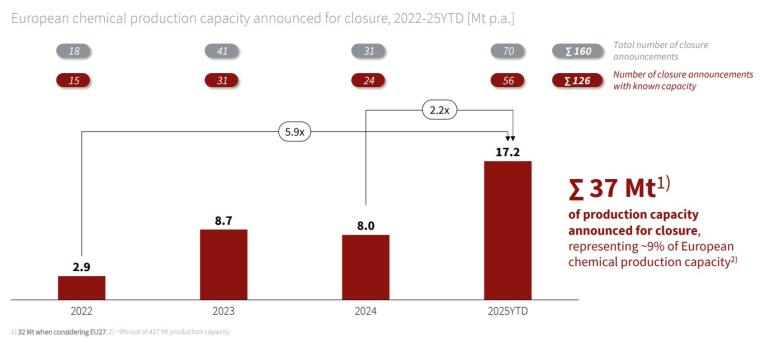

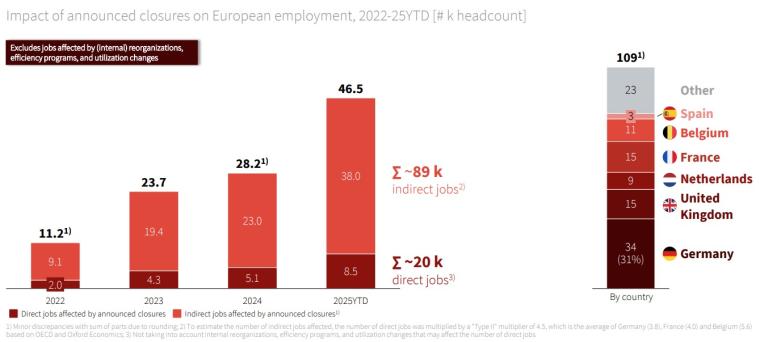

Between 2022 and early December 2025, announced chemical plant closures in Europe increased sixfold from 2.9 million tons to 17.2 million tons per year, and doubled between 2024 and 2025 alone. Total announced closures over 2022–2025 reached 37 million tons, representing about 9% of Europe's chemical production capacity. The closures have already cost 20,000 direct jobs, with 89,000 indirect jobs at risk.

Upstream petrochemicals hit hardest

Nearly half (48%) of the announced closures are in upstream petrochemicals, totaling 17.8 million tons, including nine steam crackers that represent a 16% net reduction in European steam cracking capacity. Basic inorganics account for 32% (11.7 million tons), polymers 15% (5.4 million tons), and specialty chemicals 5% (2.0 million tons). All affected crackers are located in integrated chemical clusters, putting entire industrial ecosystems under pressure.

Investment freeze signals long-term decline

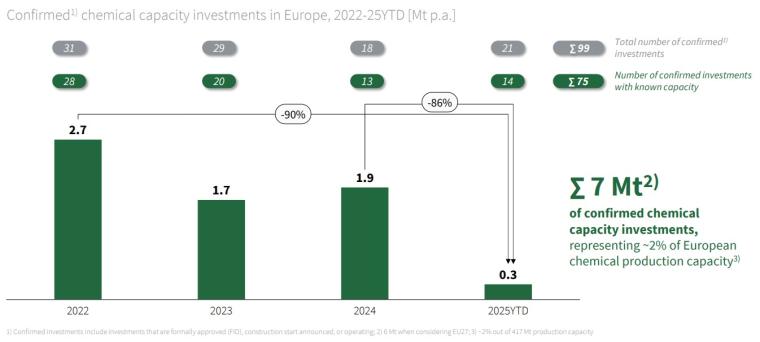

Confirmed new investments have collapsed from 2.7 million tons of capacity in 2022 to just 300,000 tons in 2025—an 86% drop in one year. Total investment capacity over 2022–2025 amounts to only 7 million tons, or about 2% of Europe's production base. Capital expenditure fell fivefold from EUR 7.6 billion to EUR 1.5 billion over the same period. The asymmetry between closures and investments points to a net capacity reduction of -30.2 million tons.

Country-level exposure varies

Germany leads with 8.8 million tons (25%) of announced closures, followed by the Netherlands (7.2 million tons, 20%), UK (4.5 million tons, 12%), France (3.9 million tons, 10%), Italy (2.5 million tons, 7%), Belgium (2.3 million tons, 6%), and Spain (1.6 million tons, 4%). Investment distribution is uneven: Belgium attracted 36% of confirmed capacity investments, while Germany received only 12%, despite being Europe's largest chemical producer.

What buyers should watch

Energy cost competitiveness is cited as the primary reason for closure in 49% of cases, followed by demand weakness (19%), overcapacity (9%), and regulatory pressure (8%). With closures accelerating and investments stalling, overseas importers should monitor supply availability for steam cracker derivatives, basic inorganics, and polymers. The trend suggests potential supply gaps and upward price pressure for these materials, particularly from German and Dutch production hubs.

Source: Read the original report | Published: February 05, 2026