Escalating geopolitical conflicts in the Middle East are driving a sharp rally in China's energy and chemical futures markets, with Brent crude nearing $110 per barrel and downstream products like polyethylene, polypropylene, caustic soda, and PVC posting significant gains in overnight trading. This development signals potential supply-chain disruptions and cost increases for overseas buyers reliant on Chinese chemical exports.

Market overview

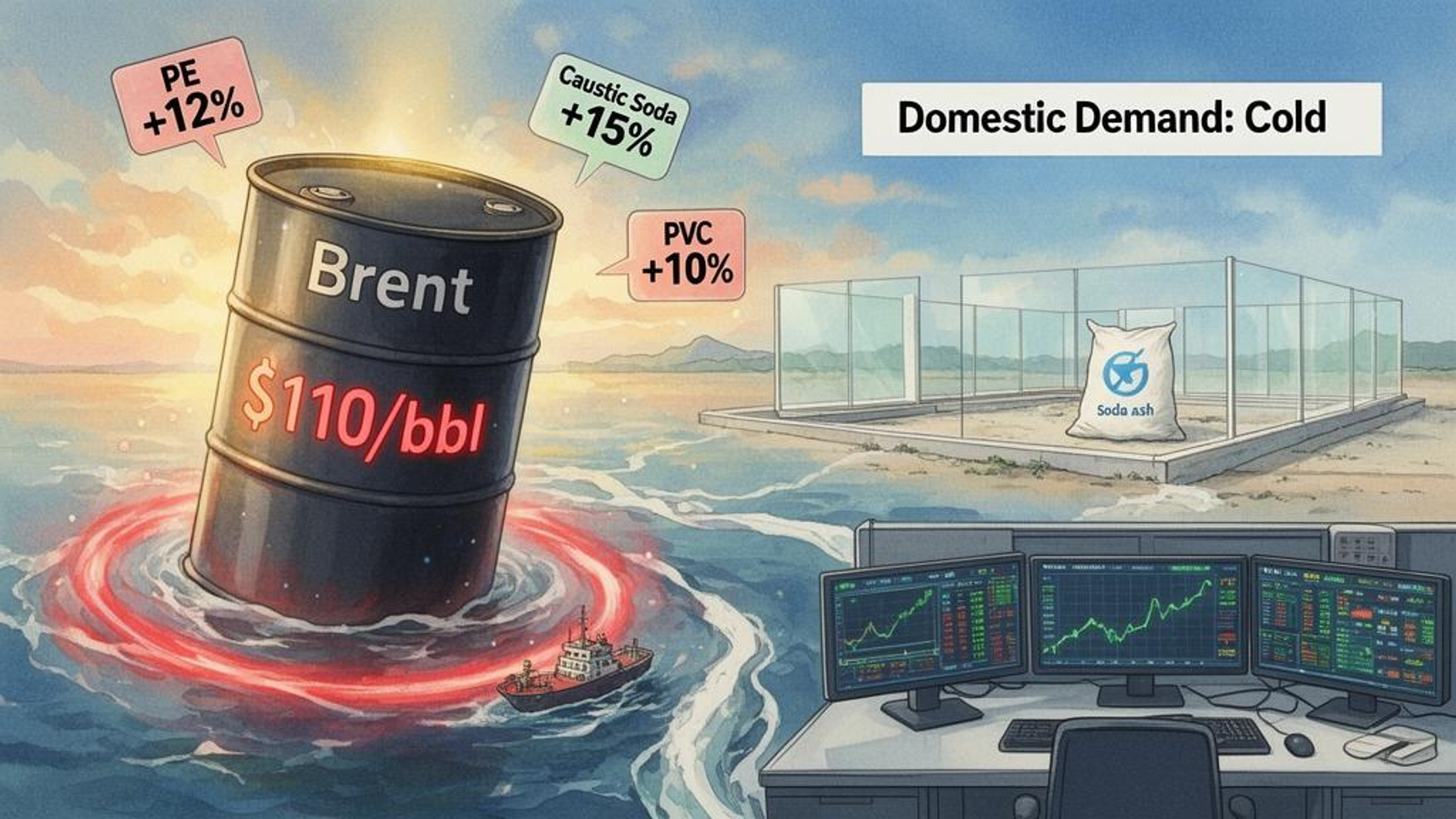

International crude oil prices surged on March 18, with Brent crude for May delivery closing nearly 6% higher at around $110 per barrel. The rally was fueled by heightened geopolitical tensions and supply disruption risks in the Middle East. In China's night trading session, polyolefins, caustic soda, and PVC futures also rebounded sharply, driven by rising feedstock costs and logistics risk premiums.

Supply-chain impact

CITIC Futures analysts noted that market sentiment is currently dominated by geopolitical factors, with most energy chemicals expected to maintain a strong range-bound trend in the short term. However, they warned of correction risks at elevated price levels. The Strait of Hormuz remains a key focus, as any disruption to shipping could severely impact global chemical supply chains, particularly for ethylene-based PVC and caustic soda.

Polyolefins and caustic soda lead gains

Polyethylene (L2605) and polypropylene (PP2605) futures closed at 9,033 yuan/ton and 9,204 yuan/ton, respectively, in night trading. Caustic soda (SH2605) rebounded to 2,503 yuan/ton after a daytime decline. The rally is attributed to rising upstream costs and supply concerns, with potential production cuts at ethylene-based plants in China and overseas due to feedstock shortages.

What buyers should watch

Overseas buyers should monitor the Strait of Hormuz situation closely, as any prolonged disruption could tighten global supply of key chemicals like PVC and caustic soda. Chinese caustic soda exports are seeing increased inquiries from international markets, while PVC exports may benefit from reduced overseas production. However, CITIC Futures advises caution against chasing prices at current highs, recommending a strategic but vigilant approach.

Divergence in other energy chemicals

Not all chemicals are benefiting equally. Natural rubber prices saw a slight correction on March 18, with spot prices falling 400 yuan/ton for domestic latex and 300 yuan/ton for Thai mixed rubber. Soda ash and glass futures remain under pressure due to weak domestic real estate demand in China, with glass inventories up 8% year-on-year and housing completions down 27.9% in January-February.

Aromatics chain supported by costs and supply cuts

PX and PTA futures are receiving support from upstream cost pressures and supply-side disruptions. China's PX operating rate fell 5.8 percentage points week-on-week to 84.6% due to preventive maintenance. PTA prices are caught between strong cost support and weak downstream demand, while ethylene glycol (EG) faces potential inventory reductions from disrupted Middle East imports.

Market outlook

The current Chinese energy chemical market exhibits a clear "external heat, internal cold" pattern, with crude oil, polyolefins, and caustic soda driven by geopolitical risks, while soda ash and glass are constrained by weak domestic fundamentals. CITIC Futures warns that while short-term price gains are justified, investors should be cautious of sharp corrections if geopolitical tensions ease. The market's direction will largely depend on developments in the Middle East, particularly the Strait of Hormuz situation.

Source: Read the original report | Published: March 19, 2026