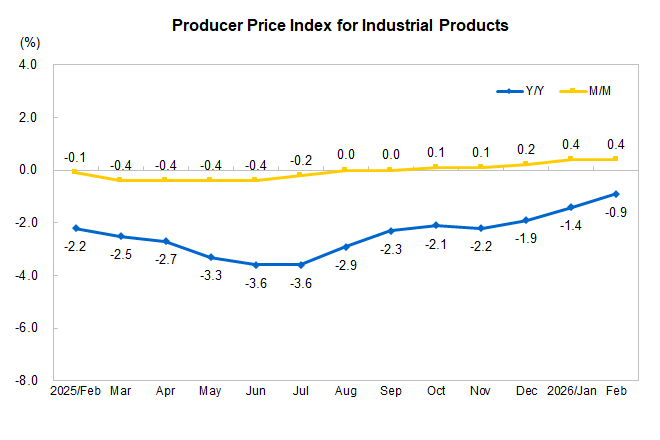

China's February 2026 Producer Price Index (PPI) data, released on March 10, shows a continued year-on-year decline of 0.9% for industrial products, with the purchasing price index for raw chemical materials dropping 5.0% year-on-year. However, nonferrous metals and cables surged 21.3% year-on-year, signaling divergent cost pressures for overseas chemical buyers sourcing from China.

Year-on-Year Price Trends

Among purchasing price indexes, fuel and power fell 8.4% year-on-year, while raw chemical materials declined 5.0%. Building materials and non-metals dropped 4.5%, ferrous metals fell 3.1%, agricultural products decreased 2.3%, and textile materials fell 1.9%. In contrast, nonferrous metals and cables rose sharply by 21.3% year-on-year.

Month-on-Month Movements

On a month-on-month basis, nonferrous metals and cables increased 4.8%, raw chemical materials rose 1.0%, textile materials gained 0.2%, and building materials edged up 0.1%. Fuel and power fell 1.2%, ferrous metals declined 0.2%, and agricultural products were flat.

Sector-Specific Highlights

In the producer price indexes for major industries, smelting and pressing of non-ferrous metals jumped 22.1% year-on-year, while extraction of petroleum and natural gas dropped 12.9%. Manufacture of raw chemical materials and chemical products fell 6.0% year-on-year, and manufacture of chemical fibers declined 12.0%.

What Buyers Should Watch

Overseas buyers of raw chemical materials should note the 5.0% year-on-year decline in purchasing prices, which may offer near-term cost relief. However, the 21.3% surge in nonferrous metals and cables signals tightening supply or strong demand in that segment. Month-on-month increases in raw chemical materials (1.0%) and textile materials (0.2%) suggest potential upward momentum. Monitoring China's PPI trends can help importers negotiate contracts and manage inventory timing.

China Sourcing Context

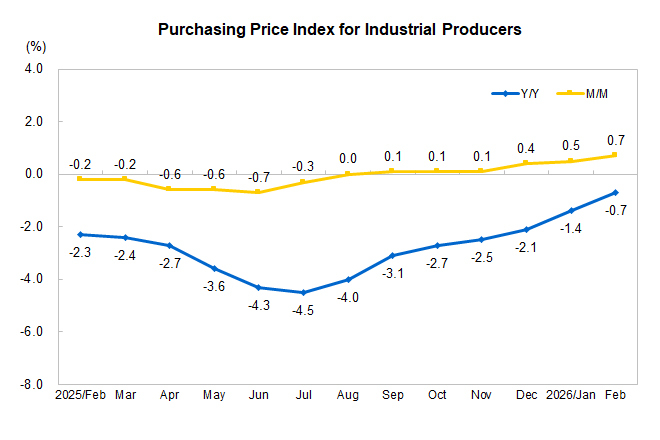

China's overall PPI decline narrowed from January, with the purchasing price index for industrial producers down 0.7% year-on-year in February, improving from a 1.4% drop in January. This stabilization, combined with mixed sector trends, indicates that chemical buyers should evaluate supplier pricing strategies carefully, especially for nonferrous-related inputs and energy-intensive chemicals.

Source: Read the original report | Published: March 10, 2026