Escalating concerns over a prolonged US-Iran conflict have triggered sharp increases in international oil prices and the costs of refined and chemical products, with analysts warning that volatility in energy and petrochemical markets is likely to persist. The situation underscores critical supply-chain risks for global buyers of industrial chemicals and fuels, particularly those reliant on Middle Eastern feedstocks.

Price surge across refining and chemicals

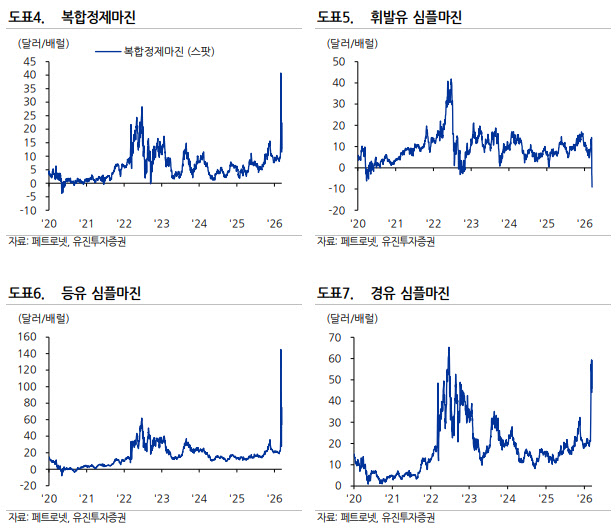

According to a report from Eugene Investment & Securities on March 17, WTI crude rose 17.2% week-on-week, with gasoline up 27.1%, diesel up 30.0%, and high-sulfur fuel oil up 32.3%. In the chemical sector, butadiene surged 35.3%, ethylene climbed 34.5%, propylene rose 28.6%, naphtha increased 27.5%, and xylene gained 27.1%. In contrast, the solar value chain showed weakness, with wafers falling 11.6% and polysilicon dropping 2.1%.

Market focus shifts to prolonged conflict scenario

The report highlights that market attention has moved beyond short-term supply disruptions to the possibility of a protracted war. Despite the partial lifting of the Hormuz Strait blockade, permission for Russian oil purchases, and the IEA's decision to release 400 million barrels of strategic reserves, sentiment is growing that the US-Iran confrontation could last longer than expected. Analysts point to Iran's Revolutionary Guard cohesion, non-dollar oil trading systems, and ties with China and Russia as factors that could reshape Middle Eastern order.

Petrochemical margins and product-specific outlook

Ethylene prices reached $1,110 per ton, propylene $1,080 per ton, and butadiene $1,915 per ton, with aromatics like benzene, toluene, xylene, and PX also strengthening. Key synthetic resins including HDPE, PP, PVC, and ABS have risen, fueling hopes for a short-term rebound in the previously sluggish chemical sector. However, the simultaneous spike in naphtha costs may lead to differentiated spread improvements across products.

What buyers should watch

Analyst Hwang Seong-hyun emphasizes that the duration of the conflict is the key variable. Alternative pipelines from Gulf producers cannot fully replace Hormuz Strait capacity, and over time, Middle Eastern crude supply chains may fall under Iranian influence. The upcoming US-China summit, expected in late March to early April, is seen as a pivotal event that could determine the next direction for oil markets and global supply chains. Buyers should monitor summit outcomes closely for potential shifts in trade and sanctions policies.

Compliance and logistics signals

Key weekly developments include prolonged Hormuz Strait blockade fears, insufficient US naval escort preparations, temporary lifting of Russian crude sanctions, IEA approval of a 400-million-barrel strategic reserve release, and implementation of domestic oil price caps. These geopolitical risks are now translating into tangible price and policy impacts, making near-term volatility across the refining and chemical sectors unavoidable.

Source: Read the original report | Published: March 17, 2026