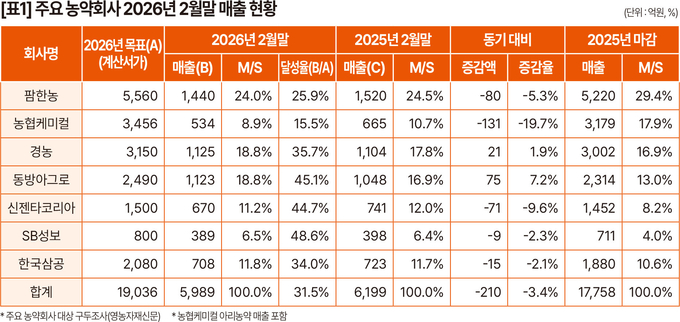

South Korea's agrochemical market started 2026 with a contraction, as combined February sales for seven major companies fell 3.4% year-on-year to KRW 598.9 billion. The downturn is driven by a 23.5% drop in Nonghyup cooperative channel deliveries, attributed to excess inventory from aggressive late-2025 sales and the Lunar New Year holiday disrupting February order-taking. This signals potential supply-chain adjustments for overseas formulators and raw-material suppliers watching the Korean market.

Sales performance of top seven firms

Aggregate sales for the seven leading agrochemical companies—Farm Hannong, Nonghyup Chemical, Kyung Nong, Dongbang Agro, Hansam, Syngenta Korea, and SB Seongbo—reached KRW 598.9 billion in February 2026, down KRW 21 billion (-3.4%) from KRW 619.9 billion a year earlier. Most firms recorded declines: Farm Hannong fell 5.3% to KRW 144 billion, Nonghyup Chemical dropped 19.7% to KRW 53.4 billion, Syngenta Korea decreased 9.6% to KRW 67 billion, Hansam slipped 2.1% to KRW 70.8 billion, and SB Seongbo edged down 2.3% to KRW 38.9 billion. Only Kyung Nong and Dongbang Agro posted gains, rising 1.9% and 7.2% respectively.

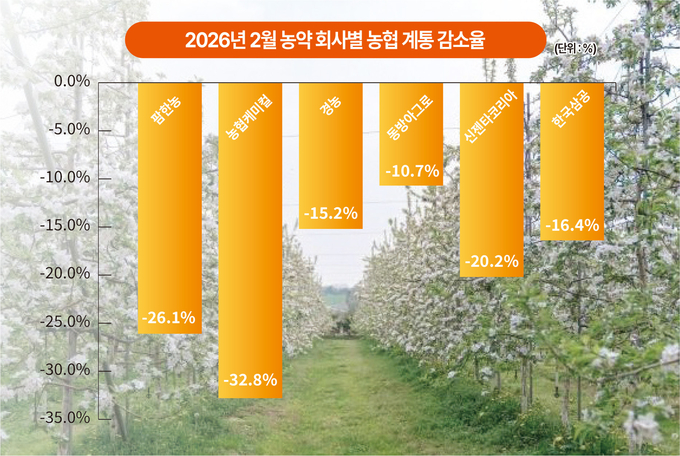

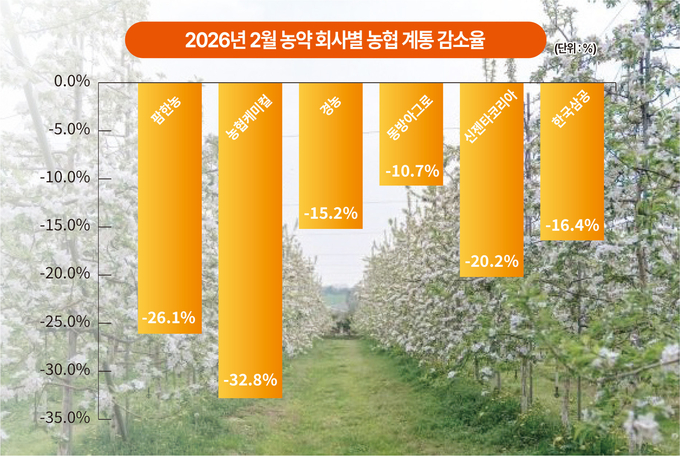

Nonghyup channel deliveries collapse 23.5%

The sharpest blow came from the Nonghyup cooperative channel, which accounts for a significant share of early-season orders. Cumulative January–February deliveries for six major firms (excluding SB Seongbo) totaled KRW 122.19 billion, down 23.5% from KRW 159.67 billion a year earlier. All companies saw double-digit declines: Farm Hannong -26.1%, Nonghyup Chemical -32.8%, Kyung Nong -15.2%, Dongbang Agro -10.7%, Syngenta Korea -20.2%, and Hansam -16.4%. Industry sources say excess inventory built up during aggressive Q4 2025 sales prompted cooperatives and retailers to cut initial orders.

Lunar New Year disrupts critical February ordering window

February is typically the peak month for Nonghyup channel orders, but the Lunar New Year holiday in mid-February severely compressed the sales period. Most cooperative orders were placed only in the final week of February, limiting volume. One sales manager noted, "We usually need to work intensively from early February to secure Nonghyup orders, but the long holiday effectively halved our selling time." This seasonal disruption compounded the inventory overhang, creating a perfect storm for the market.

Cost pressures mount despite weak pricing power

Agrochemical companies face rising input costs from higher international oil prices (increasing logistics expenses) and a weaker Korean won, which raises the cost of imported technical materials. However, price increases for finished products have been capped below 2%, insufficient to cover cost inflation. Additionally, some wholesalers are importing low-cost finished products from China, intensifying price competition and disrupting market order. One industry executive warned, "With sales declining and costs rising, companies will face severe margin pressure."

What buyers should watch: March sales as a bellwether

Industry insiders view March sales as decisive for the full-year outlook, as this month typically accounts for the largest share of spring-season revenue. If March sales do not recover significantly, the entire 2026 market could contract further. Overseas suppliers of agrochemical technical materials and intermediates should monitor Korean demand closely, as inventory destocking may reduce import orders in the near term. The shift toward Chinese finished-product imports also signals changing competitive dynamics in the Korean market.

Source: Read the original report | Published: March 16, 2026