China's industrial producer price index (PPI) turned positive in March 2026, rising 0.5% year-on-year after a 0.9% decline in February, signaling a potential inflection point for chemical buyers. The purchasing price index for raw chemical materials fell 2.2% YoY but rose 2.9% month-on-month, while nonferrous metals and cables surged 22.3% YoY, creating divergent cost pressures across the supply chain.

PPI turnaround and macro context

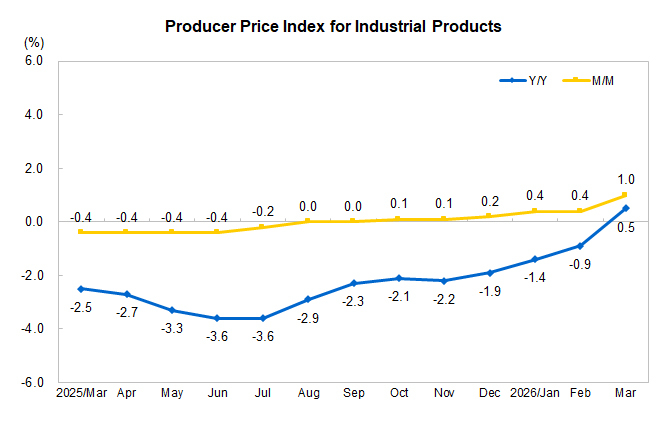

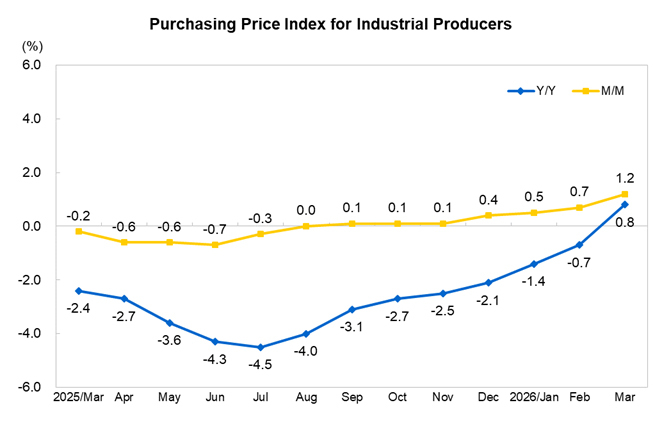

In March 2026, China's PPI for industrial products increased 0.5% year-on-year, reversing a 0.9% decline in the previous month. Month-on-month, the index rose 1.0%, accelerating by 0.6 percentage points. The purchasing price index for industrial producers also turned positive, up 0.8% YoY after a 0.7% decline, with a 1.2% month-on-month gain. For the first quarter overall, the PPI declined 0.6% YoY and the purchasing price index fell 0.5% YoY.

Raw chemical materials and key input prices

Among purchasing price indexes, raw chemical materials fell 2.2% year-on-year but rose 2.9% month-on-month. Fuel and power dropped 3.8% YoY while increasing 3.6% MoM. Building materials and non-metals declined 4.4% YoY. Ferrous metals fell 2.3% YoY. In contrast, nonferrous metals and cables surged 22.3% YoY and rose 1.5% MoM, reflecting sustained tight supply.

Sector-level price movements

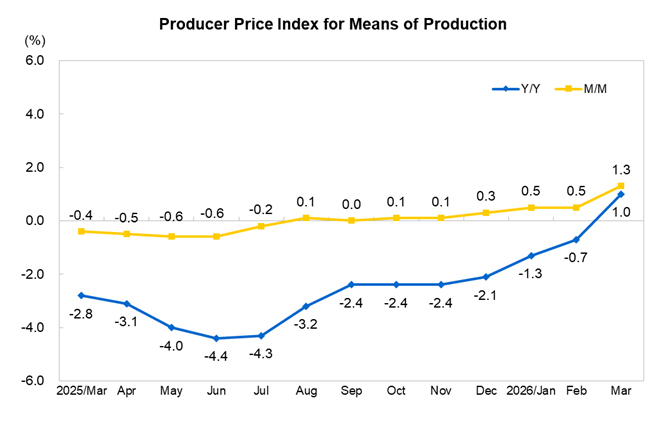

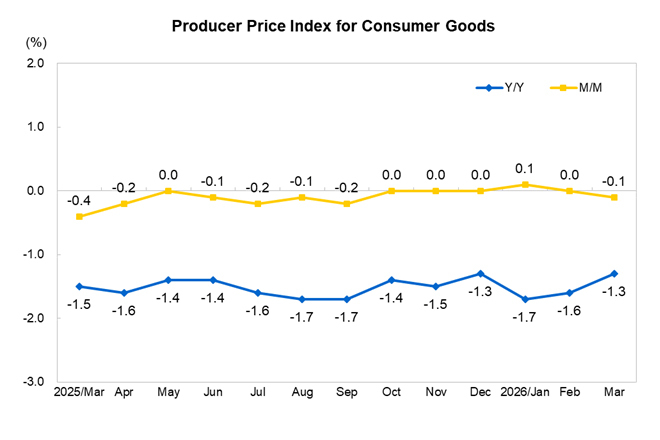

In the producer price indexes, mining and quarrying rose 2.0% YoY and 3.9% MoM. Raw materials increased 1.1% YoY and 2.4% MoM. The processing industry rose 0.9% YoY but only 0.5% MoM. Consumer goods prices declined 1.3% YoY, with food down 1.7% and durable consumer goods down 1.0%. Among major industries, smelting and pressing of non-ferrous metals jumped 22.4% YoY, while manufacture of medicines fell 4.6% YoY.

What buyers should watch

Chemical importers should note the month-on-month acceleration in raw chemical material costs (up 2.9% MoM) after a prolonged YoY decline, which may signal a bottoming process. The sharp divergence between nonferrous metals (+22.3% YoY) and building materials (-4.4% YoY) suggests selective cost pressures. The PPI turning positive after eight months of decline could indicate improving industrial demand, but consumer goods deflation (-1.3% YoY) points to weak end-user pricing power.

China sourcing context

China's March 2026 data shows the purchasing price index for raw chemical materials at -2.2% YoY, compared to -4.3% for the first quarter. The month-on-month increase of 2.9% is the largest among major input categories after fuel and power. This suggests chemical feedstock costs are recovering from deep deflation. Buyers negotiating medium-term contracts may face upward price pressure in coming months, particularly for nonferrous-related chemicals and intermediates.

Source: Read the original report | Published: April 11, 2026