China's impending export restriction on sulphuric acid, combined with Middle East geopolitical tensions disrupting sulphur flows through the Strait of Hormuz, has sent global prices soaring. For overseas buyers in mining, fertiliser, and chemical processing, this signals a structural realignment that may take months or years to normalise, with immediate implications for supply security and cost.

Price surge and market impact

China's domestic sulphuric acid price nearly doubled from $149 per metric tonne in early March 2026 to $307 per metric tonne by mid-April 2026, a 106% increase in just six weeks. India, another major importer, saw prices rise from $149 to $278 per metric tonne over the same period, an 87% jump. These movements are not transient but indicate a deeper structural shift in global acid supply chains.

China's export restriction rationale

China, historically the world's dominant sulphuric acid exporter, plans to restrict exports effective May 2026. The policy aims to protect domestic downstream industries—particularly fertiliser, chemical processing, and metal leaching—from upstream raw material constraints caused by disrupted sulphur imports via the Strait of Hormuz. Chinese producers are prioritising domestic supply over export commitments.

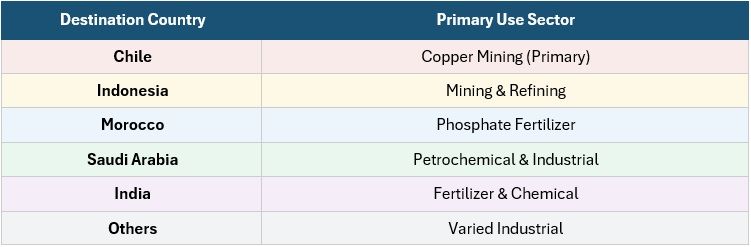

Export destination exposure

Chile faces the most acute exposure, accounting for 32% of China's sulphuric acid exports. Its copper mining industry relies on Chinese acid for heap leaching low-grade oxide ores. Indonesia (15%) faces disruptions to nickel refining, Morocco (12%) to phosphate fertiliser production, Saudi Arabia (12%) to downstream chemical processes, and India (9%) to fertiliser supply and pricing.

Downstream industry ripple effects

Sulphuric acid is critical for phosphoric acid production, which feeds DAP and MAP fertilisers. Countries like Morocco, India, and Southeast Asia face reduced fertiliser output or higher input costs. The chemical processing sector—including titanium dioxide, hydrofluoric acid, and petroleum refining—also faces cost pressure and potential production bottlenecks.

What buyers should watch

Buyers should monitor China's domestic sulphuric acid production recovery, which could ease export restrictions selectively for long-term trading partners. Prices may breach $350 per MT as sulphur inventories deplete. Formal export restrictions or force majeure declarations are expected. Diversifying sourcing and securing contracts with Chinese producers early will be critical.

Source: Read the original report | Published: April 13, 2026